Get Started With

servzone

Overview

Peer to Peer (P2P) is essentially an online platform that works for the purpose of raising debt to repay with intrigue. The borrower can be either an individual or a legitimate entity. The online platform can determine the cost of financing to be levied on loans or it can usually be chosen between the parties. Peer to peer lending has become the primary and comfortable choice of most start-ups and entrepreneurs during the early days of their business when they are looking for venture funding. At this stage, business people can get money from people without any stretch.

Peer to peer lending is a strategy for financing obligations under which people can borrow or borrow money without the contribution of any monetary organization as an intermediary. Peer to peer lending companies are directed by the Reserve Bank of India. They operate online, making P2P lending a cost-effective strategy. The P2P lending platform is a smart way to lend or borrow money. This has proved to be beneficial for both parties in such a way that lenders can make a profit by lending their money at a higher interest rate while lenders avail a lower rate of interest.

P2P lending stages are innovation-driven organizations that are listed under the Companies Act. They move between lenders and borrowers as an aggregator. In the P2P lending phase, the lender and the borrower register themselves on the site. From that point on the P2P lending platform performs due diligence and verifies applications to assist in lending / taking action.

In order to do P2P lending business, a license from the Reserve Bank of India is required. To obtain a P2P lending license, a valid application is filed with the authority with the necessary documents by the experts.

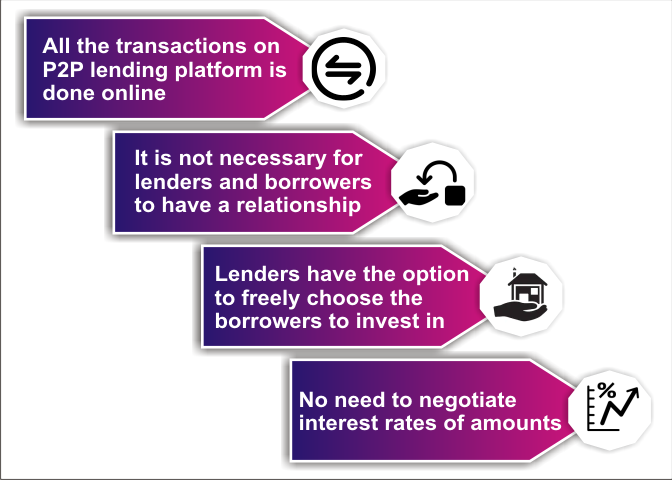

Characteristics

The P2P lending model is having a huge impact on the activities of the global financial market, in fact many finance related industries are re-shaping themselves over the past few years by introducing new modules and lending services.

The custom designed P2P lending platform is the best option as opposed to the old-fashioned way of obtaining cash from banks as banks make long efforts to support loans. Instead of moving to banks and applying for credit, P2P lending steps can be used where we simply need to deliver the necessary data from the comfort of our home / office and our advance preparation within hours And will be approved.

- All transactions are done online on P2P lending platform

- Lenders and borrowers do not have to have a relationship

- Lenders have the option to choose borrowers independently

- There is no need to negotiate interest rates or amounts.

Benefits

For Borrowers

- Low interest rates Borrowers can reap the benefits of lower loan costs when contrasted with banks and credit cards. Many times a decrease of about 35% has been observed.

- Fast application processing

Since P2P lending is done on a digital platform that makes the entire process of transactions faster and simpler.

- Fixed rate of interest

The P2P lending platform supports fixed rates even when faced with late payment cases. Therefore, many borrowers find this platform an attractive and beneficial option.

- Low fee

The P2P lending platform charges a lesser amount of fees.

For lenders

- Higher Return

Larger and, the benefits offered to investors are higher, contingent on the kind of risk you try.

- Direct communication with the buyer

The platform gives lenders the option to speak legitimately with borrowers and terminate their arrangement with borrowers.

- Diversification

Investors are filled with a variety of options to invest in their capital.

Peer to peer lending has some consensus and are as follows:

For borrowers

- The amount of loan is much lower than that of banks

- Often you experience more borrowers and fewer lenders

- Low Security

For lenders

- Regardless of whether the credit rating assessment done by Charan is reliable, there is a concern. The associated threat is not sure.

- The P2P business is still in its initial stage, it will come up on full offer very soon.

- Returns are low as opposed to being traded on open market list finance

Procedure

Any business entity, whether private firm or public firm, is eligible to start P2P lending business, they have to apply for the P2P license to RBI to start. For this, they need to complete the following:

- The organization should be registered as a private limited company or public limited company in India with the major objective of financing;

- Least net has assets of INR 2 crores.

- Website / Mobile App Workflow

- Online application is available on RBI's site (COSMOS).

- The residence of the printed copy of the application along with the documents involved will be submitted to the RBI office.

- The permit will be allowed after an attentive review of the application and the documents associated with it.

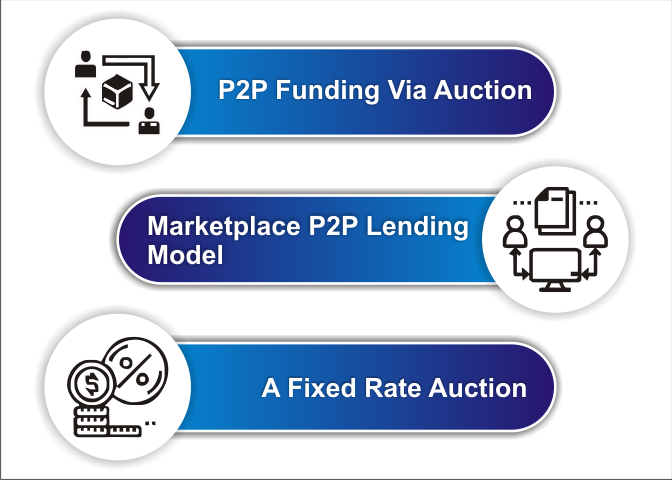

Funding Process

- P2P Funding Via Auction

Lenders in the P2P commercial center will rival each other to meet the borrower loan requirement at a minimal loan fee. The borrower loan will be subsidized by a minimum of 7-20 lenders depending on the loan amount and each piece of advance may have an optional speed of premium.

- Marketplace P2P lending model

In this model either the P2P lending platform or the money partner or platform related bank will end without anyone else and guarantee the credit condition of the borrower. When this process is over and the P2P loan phase provides loan IDs to well-meaning moneylenders.

- A Fixed Rate Auction

For this situation, the plot sum is fixed; Just the advance amount should be financed by the loan experts. This model is accurate from the commercial center's strategy.

Eligibility Criteria

- Company should be registered in India

- Applicant must have technical, entrepreneurial and managerial resources

- Therefore to complete the P2P lending platform, a candidate must have a satisfactory capital structure;

- Proposed directors have to satisfy the fit and valid model

- There should be a valid system for proficient information technology system

- A viable business plan

- Thought process to serve in the public interest

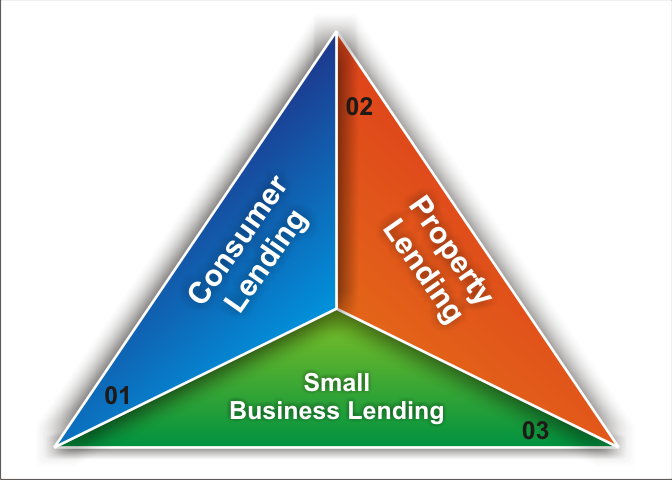

Types of Peer to Peer Lending Model

- Consumer Loans

Loans for repayment of car / weddings / holidays / home repair / credit card dues are easily available.

- Property lending

It is ensured of lending P2P against the first charge of business or personal property. Loans are obtained for making personal home loans, buy-to-let, residential restoration and commercial loans. However, this model does not have a strong fan base in India.

- Small Business Lending

Small business calls for SME loans due to the following objectives:

1. Working capital

2. Business expansion

3. Asset Finance

Working Flow

On the peer-to-peer lending platform, advances are taken by borrowers from individual financial investors (lenders) who are eager to lend their cash to borrowers at a reduced rate of interest.

On the P2P lending platform, the profiles of borrowers are shown, from where lenders can choose the profile of borrowers without having to engage in the lending process. It is not important to have a relationship between the moneylender and the buyer.

It is not fundamental that the proposed borrower gets the full loan amount, he can get a definite measure of what the financial expert (investor) asks for. For the balance, credit can be given by at least one investor in the P2P lending phase.

Reduce Risk and Maximum Return on Peer to Peer Lending Platform

In P2P lending, borrowers are being furnished in a chaotic division with a lower rate of interest than that offered by other money lenders. Under this, lenders earn higher returns than traditional betting opening offers. The financing cost incurred on credit is determined by borrowers and money lenders in the form of a dynamic loan fee different from one stage loan fee to another.

Ways to benefit returns

- To get the benefit of more significant returns, broaden the investment.

- Gains from the power of compounding and by regularly making reinvestment payments.

- To limit defaults, splits and large speculations and loans for different borrowers inside the same classification.

GST Registration

PVT. LTD. Company

Loan

Insurance